Getting Your Financial Foundation Rock Solid First

Before diving headfirst into the exciting world of stocks and bonds, there’s something absolutely essential you need to address: your financial foundation. Think of it like building a house – you wouldn’t start with the roof, right? Investing follows the same principle. A solid foundation is the key, even if it’s not the glamorous part you see plastered all over social media. Trust me, it’s this groundwork that separates those who panic sell during market downturns from those who ride them out with confidence.

Emergency Funds: Your Financial Safety Net

First things first: your emergency fund. This isn’t just spare change; it’s your financial safety net, your peace of mind. Aim for about 3-6 months of essential living expenses. I know, that might sound like a huge amount. When I was starting out, I felt the same way. My trick? I broke it down into smaller, weekly savings targets. It felt much less overwhelming than staring down one massive number. Having this fund gives you the breathing room to handle unexpected life events – a sudden car repair, a job loss, or an unexpected medical bill – without derailing your investment strategy or resorting to high-interest credit card debt.

Good Debt vs. Bad Debt: Know the Difference

Next up, let’s talk debt. Not all debt is created equal. There’s “good debt,” like a mortgage or sometimes student loans, which can potentially help build wealth over time. Then there’s “bad debt,” like those pesky high-interest credit card balances, which can drain your resources faster than you can say “interest rate.” My personal rule of thumb? Attack high-interest debt aggressively before even considering investing. If your credit card interest rate is, say, 18%, it’s going to be incredibly difficult to consistently earn returns that beat that. Check out this article on How to Build Long-Term Wealth and Achieve Financial Freedom for more insights.

Budgeting and Saving: Not as Scary as You Think

Finally, create a budget that actually works for you. There are countless apps and budgeting methods out there – Mint and YNAB are popular choices – so experiment and find what clicks. Personally, I like setting clear spending categories and tracking everything, even the small stuff. Knowing where your money goes is incredibly empowering. It helps you make informed choices about saving and investing. Speaking of saving, aim for a consistent savings rate. Even small amounts invested regularly can snowball over time thanks to the magic of compounding.

Investment Readiness Checklist

Before you jump into investing, take a look at this checklist to see how prepared you are. It compares essential financial milestones with goals that are nice to have but not mandatory before starting your investment journey.

| Financial Goal | Priority Level | Recommended Amount | Why It Matters |

|---|---|---|---|

| Emergency Fund | High | 3-6 months of expenses | Covers unexpected costs, prevents dipping into investments |

| High-Interest Debt Payoff | High | Pay off completely | Avoids paying exorbitant interest, frees up cash flow for investing |

| Budget Created | High | N/A | Provides a clear picture of income and expenses, identifies areas for savings |

| Savings Goal Established | Medium | Varies based on goals | Ensures consistent progress toward investment goals |

| Retirement Accounts (401k, IRA) | Medium | Contribute regularly | Takes advantage of tax benefits, builds long-term wealth |

This checklist helps you prioritize the most important steps. Building a secure financial base is crucial for long-term success.

The U.S. economy is projected to grow at around 2.0% in 2025. This steady growth, influenced by tight monetary policy, is expected to create a stable environment for capital markets, as discussed here. A stable economy can provide fertile ground for your investments to flourish. By building a solid financial base now, you’ll be perfectly positioned to take advantage of these opportunities when you’re ready to start investing.

Making Sense of Investment Options Without the Wall Street Jargon

So, you’ve built a solid financial base – nice work! Now for the fun part: deciding what to invest in. Let’s skip the confusing Wall Street jargon and talk plainly about how different investments work.

Understanding the Basics: Stocks, Bonds, and Funds

Think of stocks as owning a tiny slice of a company. When you buy Apple stock, you own a small piece of Apple. If Apple thrives, your stock value goes up. If Apple struggles, your stock value might go down. Bonds, on the other hand, are like IOUs. You lend money to a government or company, and they promise to pay you back with interest. They’re generally seen as less risky than stocks.

Then we have mutual funds and exchange-traded funds (ETFs). Imagine a basket holding different stocks or bonds. That’s what these are. They let you diversify your investments easily, spreading your money across multiple companies or asset classes. This diversification is key – it’s your best protection against market swings. Instead of putting all your eggs in one basket (yikes!), you spread them out, lessening the impact of any single investment underperforming.

Diversification: Your Investment Safety Net

This brings us to a core investing principle: diversification. It’s not just a buzzword, it’s a vital strategy. Imagine investing all your money in one company, and it goes bankrupt. You lose everything. Ouch. But if you diversify across different companies, industries, and asset classes, the impact of one bad investment is minimized.

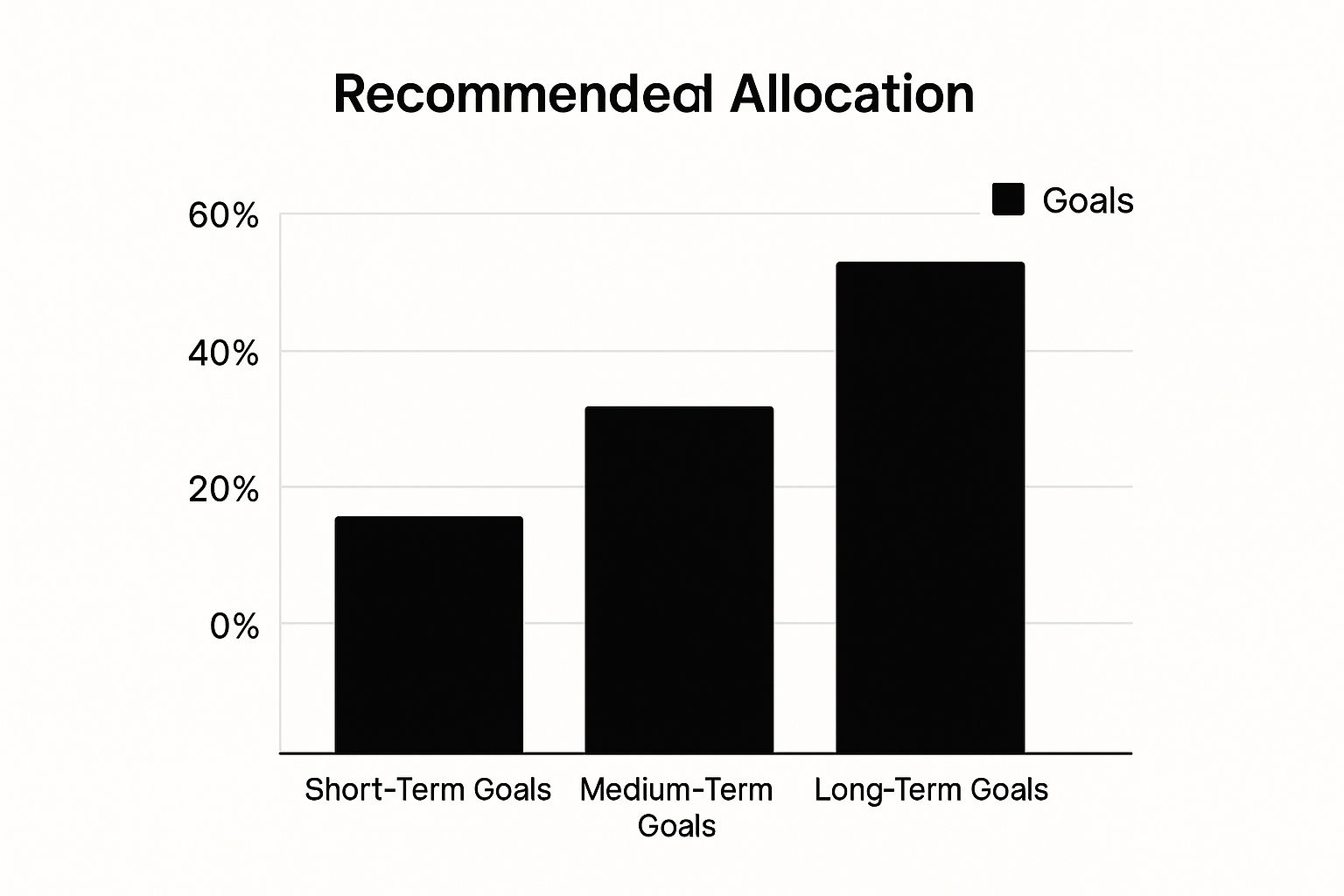

The infographic below shows a recommended asset allocation strategy for different investment goals:

As you can see, the allocation changes based on your timeframe. Short-term goals need a more conservative approach, while long-term goals can handle a higher percentage in potentially higher-growth investments like stocks.

Before we move on, let’s look at a comparison of different investment types. The table below provides a quick overview of risk, potential return, and who each investment might be best suited for.

Investment Types Comparison

| Investment Type | Risk Level | Expected Return | Liquidity | Best For |

|---|---|---|---|---|

| Stocks | Medium to High | High | High | Long-term growth, higher risk tolerance |

| Bonds | Low to Medium | Moderate | High | Income generation, lower risk tolerance |

| Mutual Funds | Varies (depends on holdings) | Varies | High | Diversification, professional management |

| ETFs | Varies (depends on holdings) | Varies | High | Diversification, low fees |

| Real Estate | Medium | Moderate to High | Low | Long-term investment, tangible asset |

This table gives you a starting point for comparing different options. Remember, your own research and due diligence are essential before making any investment decisions.

Risk and Return: Two Sides of the Same Coin

Remember, higher potential returns typically involve higher risk. Chasing hot investment tips or relying on social media gurus rarely ends well. Building wealth is a marathon, not a sprint. It’s about making informed choices and following a solid long-term strategy. Factors like technological advancements, such as the increasing use of artificial intelligence (AI) in markets, can influence market conditions and lead to unexpected economic trends.

Long-Term Thinking: The Key to Sustainable Wealth

Successful long-term investors know slow and steady wins the race. They don’t try to time the market or chase short-term gains. They focus on building a diversified portfolio that aligns with their goals and risk tolerance. Learning more about stock market investing can help you build that foundation. They understand market fluctuations are normal. By staying disciplined and focused on the long game, they can ride out market storms and reach their financial goals.

Picking the Right Account That Won’t Cost You Thousands Later

Choosing the right investment account is a big deal. It can seriously impact how much of your returns you actually get to keep. Making the wrong choice could cost you a lot of money over time. Let’s break down the main options in plain English.

Taxable Brokerage Accounts: Simple and Accessible

A taxable brokerage account is the easiest to understand. You put money in, invest it, and pay taxes on any gains when you sell. Think of it like buying and selling anything else. The benefit here is flexibility. You can access your money at any time without penalty, which is great for short-term goals or if you anticipate needing the funds soon.

Tax-Advantaged Retirement Accounts: Saving on Taxes

Tax-advantaged accounts are designed specifically for retirement. These come with nice tax perks, but also a few rules. The most common are 401(k)s, Traditional IRAs, and Roth IRAs. They all aim to lower your tax bill, either now or in the future.

401(k)s: Employer Matching Can Be a Game Changer

Many employers offer 401(k) plans. Your contributions are often tax-deductible, lowering your current taxable income. The best part? Some employers offer a matching contribution. This is basically free money! If your company offers a match, contribute enough to get the full amount. It’s a guaranteed return you won’t find anywhere else.

Traditional vs. Roth IRAs: Finding the Right Fit

A Traditional IRA is similar to a 401(k) in terms of tax benefits. Your contributions might be tax-deductible, but you’ll pay taxes when you withdraw the money in retirement. A Roth IRA works differently. You contribute after-tax money (no upfront deduction), but your withdrawals in retirement are tax-free! Which one is better for you depends on your personal circumstances. If you expect to be in a higher tax bracket in retirement, a Roth IRA is generally the smarter move.

Real-World Example: The Long-Term Impact of Tax Savings

Imagine investing $5,000 a year in a Roth IRA for 30 years, with an average 7% return. In a taxable account, you’d pay taxes on those gains every year. With a Roth, your qualified withdrawals are tax-free, which can save you a substantial amount of money over the long run.

Here’s a look at a popular fund for long-term investors: the Vanguard Total Stock Market Index Fund Admiral Shares (VTSAX):

This shows key info like the expense ratio and past performance. That low expense ratio is a big plus for long-term investors since it directly affects your returns. For a more detailed look at index funds and long-term growth, check out this article: Index Fund Benefits for Long-Term Investors. Choosing the right account and investing in low-cost options like index funds can significantly boost your investment returns over time. Understanding each account type will empower you to make a smart decision that aligns with your goals, whether it’s a comfortable retirement or another financial milestone.

Building Your Investment Strategy Without a Finance Degree

Let’s ditch the idea that investing is all about complex spreadsheets and obsessive market watching. It’s not. This section is all about building a smart investment strategy, even if you don’t have a background in finance. Think of me as your investing buddy, breaking it down in simple terms.

The Power of Index Funds: Simplicity and Growth

Ever heard of index funds? They’re incredibly popular, and for a good reason. They offer a straightforward, low-cost way to invest in a diversified portfolio of stocks or bonds. Imagine owning a tiny slice of the entire stock market instead of trying to pick individual winners and losers. This is the beauty of index funds. Even Warren Buffett sings their praises, and plenty of financial experts recommend them, especially for beginners. They take the guesswork out of stock picking and spread your risk across the board.

Dollar-Cost Averaging: Your Secret Weapon Against Market Timing

We’ve all heard stories about people “timing the market”—buying low and selling high. Sounds amazing, right? The problem is, it’s incredibly difficult to pull off consistently. It’s a bit like trying to predict next week’s lottery numbers. A far better approach is dollar-cost averaging. This means investing a set amount of money regularly, no matter what the market is doing. When prices are down, you’ll naturally buy more shares, and when they’re up, you’ll buy fewer. This helps smooth out market ups and downs over time and could even lower your average cost per share.

Asset Allocation: Finding the Right Mix for Your Goals

Asset allocation is simply how you divide your investments between different asset classes, like stocks and bonds. The best mix for you depends on things like your age, how much risk you’re comfortable with, and your investment goals. A younger investor with a longer time horizon can typically handle more risk, while someone closer to retirement might be more cautious. There are some easy rules of thumb to get you started, like the 110 minus your age rule. This suggests subtracting your age from 110 to find the percentage of your portfolio you should allocate to stocks. So, a 30-year-old might have 80% in stocks and 20% in bonds.

Interestingly, while public markets have experienced their share of volatility, private market investing has shown resilience. Investments in private markets have seen significant growth, and many investors are looking to increase their allocation in this area. You can learn more about private market trends here. While private markets might not be readily accessible to new investors, it highlights the importance of keeping up with broader investment trends.

Staying the Course: Avoiding Emotional Decisions

Once you’ve got your investment strategy in place, the most important thing is to stick with it, even when the market gets bumpy. The financial media often thrives on keeping investors on edge and encouraging frequent trading. Don’t fall into that trap. Avoid making emotional decisions based on short-term market swings. Regularly rebalancing your portfolio to maintain your target asset allocation is smart, but avoid making big changes out of fear or greed. Remember, a well-diversified portfolio and consistent contributions are the keys to long-term success. You might need to adjust your strategy occasionally based on major life changes or shifts in your financial goals, but constant tinkering is usually not helpful.

Choosing Investment Platforms That Actually Serve You

So, you’ve got a handle on investment strategies. Great! Now let’s talk about where you’ll actually buy and sell those investments: investment platforms, sometimes called brokerages. Choosing the right one is a big deal. It can make investing a breeze or a real pain. I’ve been around the block with a few different platforms, and I’m happy to share what I’ve learned.

The Big Players: Fidelity, Vanguard, and Schwab

You’ve probably heard of the big three: Fidelity, Vanguard, and Charles Schwab. They’re all solid choices, especially for beginners. They offer a wide range of investments, helpful resources, and generally decent customer service. They’re also well-established and reliable, having been around for quite a while. Plus, the competition between them has kept fees low, which is a win for us!

Newer Platforms: Robinhood and Others

Then you have the newer kids on the block like Robinhood, with their simple, mobile-first design and often zero commission trades. If you’re just starting out and want a streamlined experience, these platforms can be attractive. But be aware of their limitations. Some might not have as many research tools or access to advisor support as the bigger firms.

Fees That Matter (and Those That Don’t)

Remember when trading commissions used to be a huge expense? Now, most major platforms offer commission-free trading for stocks, ETFs, and options. But other fees can still sneak up on you. Expense ratios for mutual funds and ETFs, for example, are annual fees charged by fund managers. These can really eat into your returns over the long haul. So, don’t just look at commissions. Check those expense ratios, too! Even small differences can add up over time.

Here’s a look at what Fidelity offers for index funds:

This screenshot shows Fidelity’s index fund resources – a great starting point for new investors. The key takeaway? There are tons of index funds out there now, making this investing approach incredibly accessible.

Robo-Advisors vs. DIY Investing: Which is Right for You?

Think about how involved you want to be in managing your investments. If you prefer a hands-off approach, a robo-advisor might be a good fit. These automated platforms build and manage your portfolio based on your goals and risk tolerance, usually for a small annual fee. If you enjoy researching and making your own decisions, the DIY approach on a traditional brokerage platform is probably better for you.

Getting Started: Opening Your Account and Making Your First Investment

Once you’ve picked a platform, opening an account is usually pretty simple. You’ll provide some basic info and link your bank account. Funding your account is quick and easy, too. Then, you’re ready to start investing! One trap many new investors fall into is analysis paralysis. They overthink everything and get stuck in the research phase. My advice? Start simple. Pick a diversified portfolio of index funds or ETFs. You can always adjust your strategy as you go.

Insider Tips to Avoid Common Beginner Mistakes

Here are a few tips to help you avoid some common pitfalls:

- Don’t invest money you’ll need soon. The market can be unpredictable, and you don’t want to be forced to sell at a loss if you suddenly need the cash.

- Start small and gradually increase your investments. This helps you get comfortable with the process without risking too much at once.

- Don’t chase hot tips or try to time the market. Focus on a long-term strategy, not short-term gains.

- Use the educational resources available. Most platforms have tons of helpful info and tools.

- Don’t be afraid to ask for help. If you’re unsure about something, contact the platform’s customer service or talk to a financial advisor.

Choosing the right investment platform and avoiding these common mistakes can make a huge difference in your investing journey. Look for features that fit your needs and investing style. This sets you up for a positive and rewarding experience.

Surviving Market Crashes Without Losing Your Mind

This screenshot from Vanguard shows some sample portfolio allocations for different risk tolerances. See how the stock percentage shrinks as things get more conservative? This is a visual reminder to match your investments with your comfort level. Market downturns are a fact of life, a normal part of the investing cycle. Your reaction to them is what separates building wealth from accidentally buying high and selling low (ouch!). Let’s talk about navigating those storms without panicking. This isn’t textbook stuff; it’s real-world advice.

Diversification: Your Best Defense

We’ve talked about diversification before, but it’s your lifeline in a crash. Spreading your investments across different things – stocks, bonds, real estate, etc. – and different parts of the world means one bad apple won’t spoil the whole bunch. It’s like building a house with multiple supports. One beam weakens? The others hold it up.

The Mindset Shift: Seeing Crashes as Opportunities

Experienced investors don’t see crashes as disasters; they see sales. Prices drop? It’s like your favorite store having a clearance event. Imagine grabbing Apple or Google stock at a discount! Downturns give you a chance to buy more shares for less, potentially supercharging your returns when the market bounces back.

Avoiding Emotional Traps: Staying Disciplined When Others Panic

Market crashes breed fear. You’ll hear whispers of selling everything before it’s “too late.” This is when discipline matters most. Remember your long-term game plan and ignore the emotional noise. Markets have a history of recovering, and patience usually wins.

Rebalancing: Maintaining Your Target Asset Allocation

Market swings can mess with your portfolio’s balance. A crash might suddenly lower the percentage of stocks you hold. Rebalancing means adjusting to get back to your target. This could mean selling some bonds and buying more stocks after a drop. It feels weird, but it lets you capitalize on lower prices.

Knowing When to Adjust (and When to Stay Put)

Staying the course is generally the best move in volatile markets. But life happens. A new job or a big raise might mean revisiting your investment goals and risk tolerance. Just don’t react to every market blip. Trust your long-term strategy. Consistent contributions and patience are powerful tools.

Learning to invest isn’t just about picking investments; it’s about handling the inevitable ups and downs. By embracing diversification, a smart mindset, and a disciplined approach, you can face market crashes with confidence and set yourself up for long-term success.

Your Roadmap From Beginner to Confident Investor

So, you’re ready to dive into the world of investing? Awesome! Let’s map out a plan to take you from newbie to seasoned investor, ditching the confusion and embracing the excitement.

Setting Realistic Expectations: Ditch the Get-Rich-Quick Mindset

First off, let’s be real. Forget those social media gurus promising instant millions. Building wealth is more like a steady hike than a rocket launch. It takes time, patience, and a good dose of consistency. A 7-8% annual return on a diversified stock portfolio is a solid long-term target. Don’t sweat the small dips and focus on the long game. Slow and steady wins the race, remember?

Creating Accountability: Staying Consistent Over Time

Staying on track is easier said than done. Life throws curveballs, and it’s easy to let investing slip. My trick? Automate everything! Set up automatic transfers from your checking account to your investment account every month. It’s like paying yourself first. Also, find an accountability partner. A friend, family member, or even a financial advisor can help you stay focused and motivated. Sharing your goals and checking in regularly works wonders.

Exploring Advanced Strategies: Knowing When You’re Ready

As your portfolio grows and you get more comfortable, you might be tempted to explore fancier investment strategies like sector-specific investing, options trading, or real estate. Don’t jump the gun! Nail the basics first. A solid foundation of diversified index funds or ETFs is the best starting point. Once you’re consistently hitting your goals and feel confident with the fundamentals, then consider adding some complexity.

Continuous Learning: Staying Ahead of the Curve

The investment world is constantly changing. Make learning a habit. Read books, follow trustworthy financial blogs (like InvestVibes!), and consider webinars or seminars. Staying informed helps you make smart decisions and adjust your strategy as needed. Knowledge is power, especially when it comes to your money.

Measuring Progress and Celebrating Milestones: Staying Motivated

Building wealth can feel like a long journey. It’s important to celebrate your wins along the way – hitting a savings goal, reaching a portfolio milestone, or even just staying consistent for a year. These little victories keep you motivated and reinforce good habits. Investing is a marathon, not a sprint, so enjoy the process!